10 Types of Trusts: A Quick Look for the RIA

Have you had the trust talk?

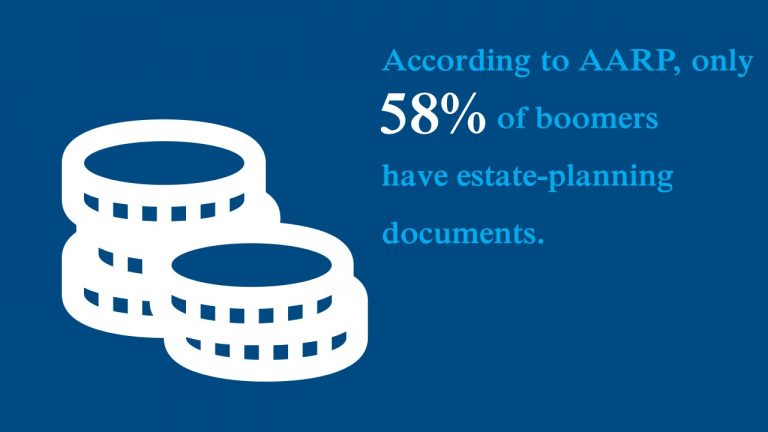

Your retired clients may be thinking about what happens to their wealth after they’re gone. Have you had an honest discussion about their estate? Family accountants and financial advisors are often the ones who know the most about a family’s dynamics. You’ve probably just about heard it all! Advisors should also work with estate-planning attorneys to ensure their clients have a solid plan in place and that their finances are secure. Today, we’re sharing some helpful information regarding trusts.

10 Common Types of Trusts

Considering the myriad of trusts available, creating an estate plan that works can seem daunting. It doesn’t have to be. Here’s a look at the basics of 10 common trusts to provide a general understanding. There will not be a quiz at the end.

Bypass Trusts

Commonly referred to as Credit Shelter Trust, Family Trust, or B Trust, Bypass Trusts do just that: bypass the surviving spouse’s estate to take advantage of tax exclusions and provide asset protection.

Charitable Lead Trusts

CLTs are split interest trusts that provide a stream of income to a charity of your choice for a period of years or a lifetime. Whatever’s left goes to you or your loved ones.

Charitable Remainder Trusts

CRTs are split interest trusts which provide a stream of income to you for a period of years or a lifetime and the remainder goes to the charity of your choice.

Special Needs Trusts

SNTs allow you to benefit someone with special needs without disqualifying them for governmental benefits. Federal laws allow special needs beneficiaries to obtain benefits from a carefully crafted trust without defeating eligibility for government benefits.

Generation-Skipping Trusts

GST Trusts allow you to distribute your assets to your grandchildren, or even to later generations, without paying the generation-skipping tax.

Grantor Retained Annuity Trusts

GRATs are irrevocable trusts that are used to make large financial gifts to family members while limiting estate and gift taxes.

Irrevocable Life Insurance Trusts

ILITs are designed to exclude life insurance proceeds from the deceased’s estate for tax purposes. However, proceeds are still available to provide liquidity to pay taxes, equalize inheritances, fund buy-sell agreements, or provide an inheritance.

Marital Trusts

Marital Trusts are designed to provide asset protection and financial benefits to a surviving spouse. Trust assets are included in his or her estate for tax purposes.

Qualified Terminable Interest Property Trusts

QTIPs initially provide income to a surviving spouse and, upon his or her death, the remaining assets are distributed to other named beneficiaries. These are commonly used in second marriage situations and to maximize estate and generation-skipping tax exemptions and tax planning flexibility.

Testamentary Trusts

Testamentary Trusts are created in a will. These trusts are created upon an individual’s death and are commonly used to provide for a beneficiary. They are commonly used when a beneficiary is too young, has medical or drug issues, or may be a spendthrift. Trusts also provide asset protection from lawsuits brought against the beneficiary.

Feel free to share this information with your clients and encourage them to ask questions. Their financial well-being is a priority, after all.

Author Bio

Leila Shaver is the Founder of My RIA Lawyer, a law firm that provides compliance and legal consulting for financial institutions. With extensive experience as a securities attorney and compliance expert, she has served as Chief Compliance Officer and General Counsel to RIAs, BDs, and TAMPs with billions in assets under management.

Leila understands the challenges RIAs face and is committed to helping RIAs streamline their processes, mitigate risks, and ensure compliance with regulatory requirements. She received her Juris Doctor from Atlanta’s John Marshall Law School and is a West Georgia Young Lawyers’ Association member. Leila has received numerous accolades for her work, including the Carroll County Bar Association’s Outstanding Young Lawyer Award in 2017.